Your finance team sees the same maintenance spend differently than your operations team does — and both are right. Whether an expense hits the income statement today or sits on the balance sheet and depreciates over five years changes your P&L, your tax position, your capital request process, and how your CFO reads your department's performance. Getting CapEx and OpEx classification wrong distorts financial statements, delays approvals, and leaves asset replacement cycles unplanned until a failure forces the decision. Start a free trial to see how Oxmaint tracks maintenance spend by category, asset, and lifecycle stage — so every budget conversation starts with data, not guesswork.

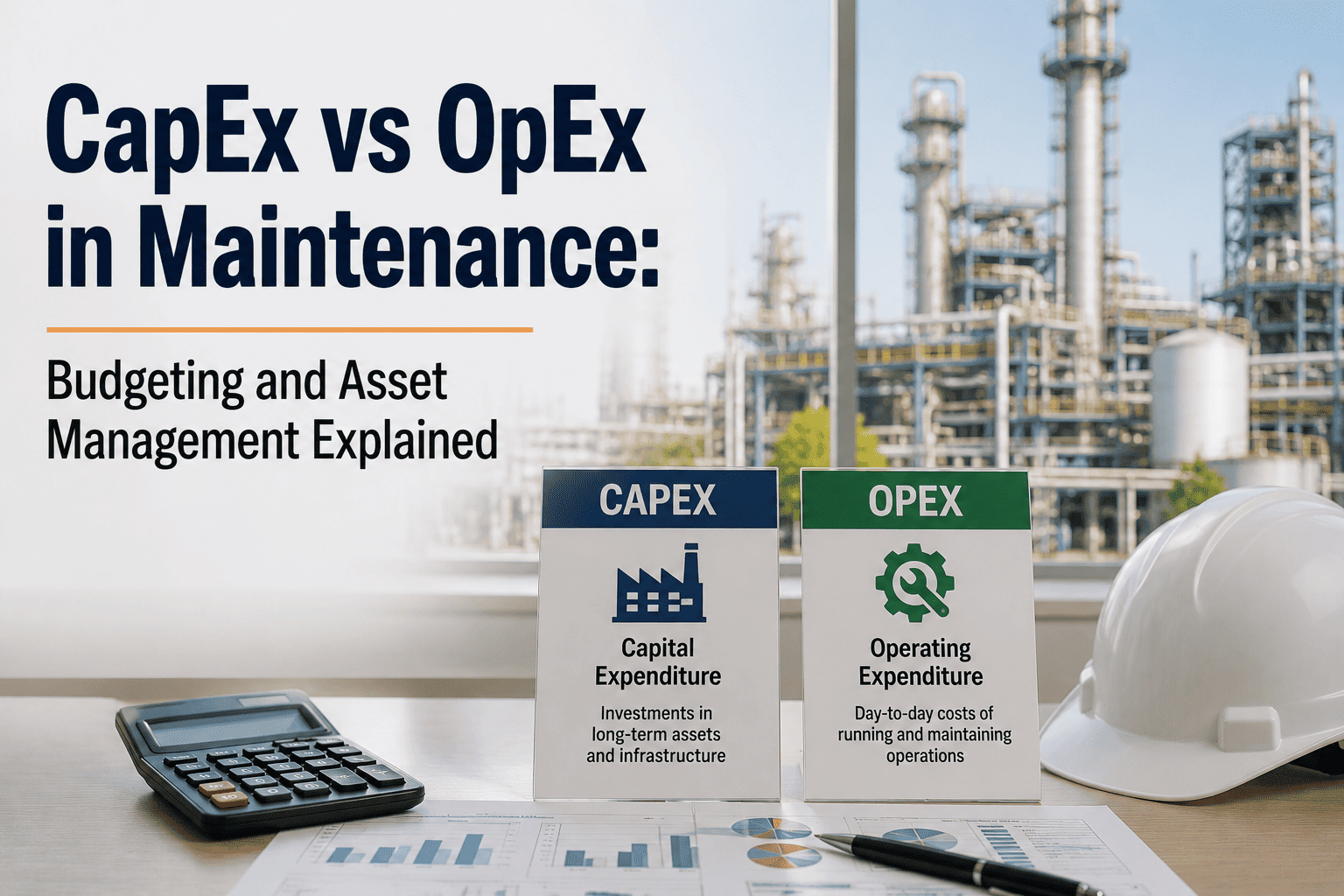

Capital Expenditure — CapEx

Long-Term Investment

Funds used to acquire, upgrade, or extend the useful life of a physical asset. Capitalised on the balance sheet and expensed gradually through depreciation over the asset's useful life — not in the period the spend occurs.

Appears on the balance sheet as a fixed asset

Depreciated over useful life (3–40 years depending on asset type)

Requires board or capital committee approval above threshold

Examples: new HVAC plant, chiller replacement, roof replacement

Operating Expenditure — OpEx

Day-to-Day Operation

Costs incurred to keep assets running at their current condition. Fully expensed in the period they occur — recognised immediately on the income statement with no carry-forward to future accounting periods.

Appears on the income statement in the current period

Fully deductible in the year incurred for tax purposes

Approved through operating budget — faster, lower threshold

Examples: filter replacements, lubricants, belt changes, inspections

Why Misclassification Costs You More Than the Expense Itself

A routine repair incorrectly capitalised inflates your asset base, understates current period expenses, and overstates profit. When auditors or tax authorities reverse the classification, the adjustment hits as a lump expense. It also delays the tax deduction you were entitled to in the year the spend occurred.

A capital improvement expensed immediately overstates operating costs, understates asset value, and skews period profit downward. Funders, lenders, and boards looking at your financials see a worse operational picture than reality — and your asset register does not reflect what you actually own.

Without a documented capitalisation threshold and classification policy, decisions are made individually by whoever is processing the invoice. The same type of repair is treated differently depending on who approved it. Financial statements become inconsistent year on year — a red flag in any audit or financing process.

The Three Rules That Determine CapEx vs OpEx Classification

Under GAAP, an expenditure on an existing asset must be capitalised if it accomplishes at least one of the following. Everything else is an operating expense in the period incurred.

Extends the Asset's Useful Life Beyond Original Estimate

If the work causes the asset to remain productive for materially longer than it would have without intervention, it is a capital improvement. Replacing a worn roof that adds 20 years of building life is CapEx. Patching a leak to restore the roof to its previous condition is OpEx. The test is: does the work extend the timeline, or just restore the current state?

Adds New Capability or Materially Improves the Asset

If the work adds a function, capability, or efficiency the asset did not previously have, it is a capital improvement. Upgrading a standard HVAC unit to a high-efficiency variable speed system is CapEx. Replacing the existing fan motor with an identical unit to restore original performance is OpEx. The test is: does the asset do something new or better, or does it just do the same thing again?

Adapts the Asset to a New or Different Use

Reconfiguring a space, repurposing equipment, or converting a system for a different function qualifies as a capital improvement — the asset is changed in kind, not just restored. Converting a diesel boiler to gas, or reconfiguring an open office plan into individual offices, meets this test. Repainting the office to the same colour does not.

The Capitalisation Threshold

Every organisation needs a documented capitalisation threshold — the dollar amount below which an expenditure is treated as OpEx regardless of what it does to the asset. Most commercial facilities set this between $2,500 and $10,000. A pump replacement costing $4,800 is OpEx at a facility with a $5,000 threshold and CapEx at one with a $3,000 threshold. The threshold must be documented in your accounting policy, applied consistently, and reviewed periodically — it is not a decision made at the point of invoice approval.

$2,500

IRS de minimis safe harbour (without applicable financial statement)

$5,000

IRS de minimis safe harbour (with applicable financial statement)

$10,000

Common threshold for building improvement capitalisation in larger facilities

Set your threshold. Document it. Apply it consistently across every work order.

CapEx vs OpEx — Real Maintenance Examples

| Maintenance Activity |

Classification |

Why |

| Replacing identical HVAC fan motor (like-for-like) |

OpEx |

Restores original condition — no extension of life, no new capability |

| Upgrading HVAC to high-efficiency variable speed system |

CapEx |

Materially improves energy efficiency — new capability beyond original |

| Annual steam trap survey and replacement programme |

OpEx |

Routine maintenance restoring system to designed operating condition |

| Full boiler replacement (end of asset life) |

CapEx |

New asset with independent useful life — capitalised and depreciated |

| Patching roof leaks, replacing individual tiles |

OpEx |

Restores existing condition — does not extend life or add capability |

| Full roof replacement (beyond end of useful life) |

CapEx |

Extends building useful life — depreciated over new roof service life |

| Lubricating bearings, filter changes, belt replacements |

OpEx |

Routine PM — keeps asset at current state, no threshold crossed |

| Lift modernisation — new controls, motor, cab finish |

CapEx |

Extends asset life and adds new safety/performance capability |

Your CMMS Should Know the Difference So Your Finance Team Does Not Have to Guess

Oxmaint tracks every work order with asset, cost category, and lifecycle stage — giving your team the data to classify CapEx and OpEx correctly at the point of spend, not three months later at year-end. Sign up free or book a demo to see the asset cost tracking workflow.

How Depreciation Works on Capitalised Maintenance

When a maintenance expenditure is correctly capitalised, it does not hit your P&L in the year of spend. Instead, the cost is spread across the asset's useful life through annual depreciation charges. Understanding depreciation is essential to building a maintenance budget that finance will approve.

Straight-Line Depreciation

Most common method for facilities

The asset cost (less any residual value) is divided equally across each year of useful life. A $120,000 chiller with a 20-year life and $0 residual generates $6,000 of depreciation expense every year — appearing on the income statement regardless of whether the asset requires any maintenance spend that year.

Formula

(Asset Cost − Residual Value) ÷ Useful Life in Years = Annual Depreciation

Typical Asset Useful Lives

For maintenance budget planning

HVAC plant / chillers

15–25 years

Roofing systems

20–40 years

Electrical systems

20–40 years

Mechanical equipment

10–20 years

Lifts / elevators

15–25 years

Building a Maintenance Budget That Works for Both Operations and Finance

Separate CapEx and OpEx in the Budget from Day One

Produce two distinct maintenance budgets: an operating budget for recurring PM, consumables, labour, and reactive repairs; and a capital budget for asset replacements, major upgrades, and end-of-life projects. Finance teams evaluate these differently — operating budgets are scrutinised on year-over-year variance, capital budgets on ROI and payback period. Conflating them leads to confusion in approval processes and makes it impossible to benchmark your operational spend against industry norms.

Build a Lifecycle Asset Register

Every major asset should have a documented installation date, expected useful life, current replacement cost estimate, and remaining life. This transforms the CapEx budget from a reaction to failures into a rolling 5–10 year forecast. Boards and finance committees approve planned capital programmes far more readily than emergency replacement requests. An asset register that shows a chiller reaching end of life in 3 years — with cost projections — gives you the runway to plan funding, apply for capital, and schedule the replacement during a low-impact period.

Track the Repair-to-Replace Tipping Point

For every major asset, accumulate the total OpEx spent on reactive repairs and corrective maintenance year by year. When cumulative repair spend approaches 50–60% of the asset's current replacement cost, continued repair is rarely economically justifiable — you are funding operating losses to avoid a capital approval conversation. A CMMS that tracks cost per asset gives you the data to make this argument with numbers, not anecdote. This is the core of the repair-versus-replace decision that defines whether your CapEx budget grows or stays flat.

Use Energy and Sustainability to Justify CapEx

Capital replacement projects that reduce energy consumption or carbon emissions can be justified on ROI grounds that pure maintenance arguments cannot reach. An eight-year payback on an efficient chiller system is a difficult capital conversation. The same project framed as energy cost savings of $40,000 per year plus carbon reduction plus avoided reactive maintenance of $12,000 per year shortens the payback period significantly and frames the spend as investment, not cost. Your CapEx requests should always include total cost of ownership analysis, not just acquisition cost.

Classify at the Work Order, Not the Invoice

The most reliable way to ensure consistent classification is to tag each work order as OpEx or CapEx at the point of creation — before the work is done — based on your documented policy. This prevents the end-of-period scramble where finance receives a stack of invoices and must classify retrospectively. A CMMS with cost category fields at the work order level removes classification decisions from the accounts payable process and puts them where the context exists: with the maintenance team that knows what the work actually did to the asset.

The CFO Conversation Every Maintenance Manager Needs to Have

Maintenance departments that operate as cost centres — with no lifecycle asset data, no repair cost history, and no capital plan — have their budgets cut first in a downturn. Departments that present a rolling 5-year capital plan, show the repair-to-replace economics on ageing assets, and quantify the OpEx reduction from capital investment get funding. The data that makes that conversation possible lives in your CMMS. Sign up to Oxmaint or book a demo to see how asset cost tracking supports the capital budget process end to end.

Frequently Asked Questions

Q

Can preventive maintenance be capitalised?

Generally, no. Routine preventive maintenance — inspections, filter changes, lubrication, calibration — is OpEx because it keeps the asset at its current operating condition without extending its useful life or adding new capability. The IRS Routine Maintenance Safe Harbour explicitly exempts amounts paid for routine maintenance from capitalisation requirements. Where PM work results in a component replacement that does extend life or add capability above your capitalisation threshold, that specific component replacement may be CapEx while the labour and inspection elements remain OpEx.

Q

What happens to the old asset when we replace it as CapEx?

The replaced asset must be retired from the asset register. Its net book value — original cost less accumulated depreciation at the point of retirement — is recognised as a disposal loss (or gain if proceeds from salvage exceed net book value). Failing to retire the old asset and simply adding the new one creates phantom assets on the balance sheet and inflates depreciation charges. Your asset register should record disposal date, method, and proceeds for every retired capital asset.

Q

Does a CapEx project include the labour cost of installation?

Yes. Under GAAP, all costs necessary to bring a capital asset to its intended condition and location are capitalised — including installation labour, freight, site preparation, and commissioning costs. Internal labour used for installation can also be capitalised if the hours are specifically tracked to the project. Labour for the ongoing operation or maintenance of the asset after it is placed in service is OpEx. The cutoff is the date the asset is ready for its intended use — costs before that date are capitalised, costs after are expensed.

Q

How does a CMMS help with CapEx vs OpEx management?

A CMMS provides three capabilities that directly support CapEx and OpEx management. First, cost tracking per asset — every work order cost is linked to a specific asset, enabling cumulative repair cost analysis that informs the repair-versus-replace decision. Second, lifecycle visibility — installation dates, maintenance history, and cost trends by asset give finance teams the data to depreciation schedules and capital forecasts. Third, classification discipline — work orders tagged as OpEx or CapEx at creation produce clean cost category data that goes directly into budget reporting without manual reclassification.

Turn Your Maintenance Spend Into a Board-Ready Asset Strategy

Oxmaint tracks every work order cost against its asset, captures CapEx and OpEx classification at the point of creation, and builds the lifecycle cost history your finance team needs for capital planning. Asset register, repair cost trends, replacement forecasts, and PM scheduling in one platform — live in days, not months.